21. - 16 - MDAs, be invited to the presentation of Systems and Processes Review and Monitoring for compliance reports. 4. The Management of the Ministry be issued with a W arning L etter by the ACC to remind them of their obligation to comply.

2. ii | P a g e Scan this QR Code to go to the ACC Website

4. iv | P a g e TABLE OF FIGURES Figure 2: The Compliance Score of the MoSW Includin g the ................................ .... - 7 - Figure 3: The Compliance Score of the MoSW excludin g the 5 Inapplicable 5 Recommendations ................................ ................................ ................................ .. - 8 - Figure 4: Double Column Chart showing the Compliance Levels of the various thematic Areas ................................ ................................ ................................ ..................... - 9 -

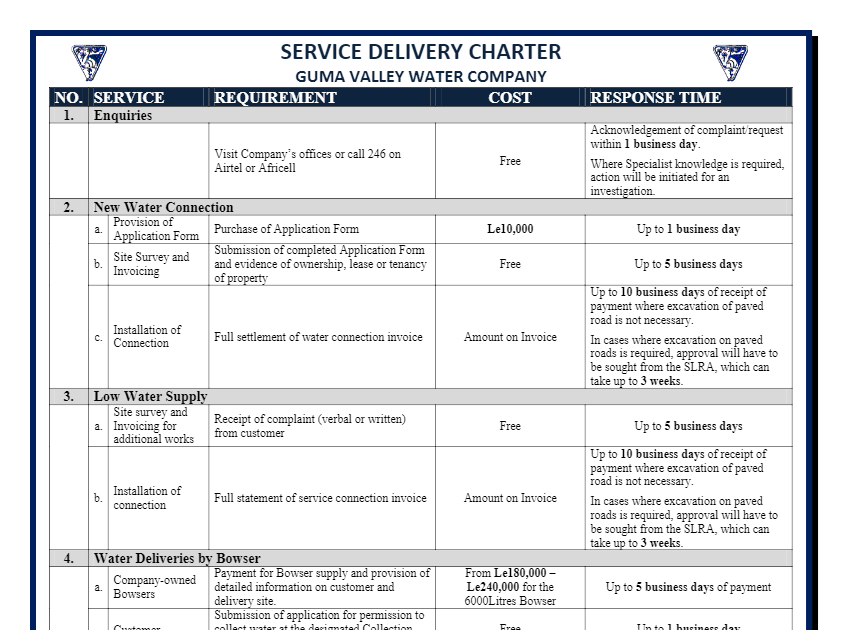

17. - 12 - Finally, the Le44 , 000,000.00 owed to Chel e sco C ompany had still not been paid . A request was made by the project engineer to the MoF for the payment of the said amount. But it was not honored by MoF because the MoF will only consider the payment of debts that were to the tune of Le 1 billion and above. 7 . 7 Fuel Management Only one 1 (25%) out of four (4) recommendations proffered in the Fuel Management Indicator was fully implemented . It was therefore important to note that the Ministry had not taken the implementation of ACC recommendations relating to fuel management seriously. The recommendation adhered to had to do with the pro vision of Fuel Accountability tools; for which all the samples collected proved full compliance. On the contrary, the recommendation regarding the robustness of fuel reconciliation report and tracking plan was not fully implemented, Management though the F inance D epartment had developed a fuel policy, which was expected to be implemented in such a way that fuel can be used judiciously through a robust fuel reconciliation and tracking plan. No action had been taken by the Ministry to implement the recommend ations relating to; accountability of the excess of 285 liters of fuel misuse d and the variance of Le129,377,000 resulting from the difference between expenditure on fuel and verified amount by the Review T eam. 7 .8 Stipend to C ontract S taff The only recommendation proffered in respect of this indicator has been fully implemented , recording 100% compliance. Now, other than the regular salaries of staff, no stipend was paid to regular staff. The project for which stipend was paid had been transferred to GUMA and SALWACO and the M inistry only provided a supervisory role .

8. - 3 - 1.0 INTRODUCTION/BACKGROUND In line with Section 8 (1) of the ACA 2008 as amended in 2019, the Monitoring and Compliance Unit of the ACC have completed a detailed monitoring for compliance with SPRR at the MoWR . The purpose of the monitoring intervention was to gauge the compliance score or status of the Ministry in the implementation of ACC’s SPRR as enshrined in section 8. (1) of the ACA 2008 as amended in 2019. The MoWR was established in January 2013 to formulate and implement policies for the development and management of water resources, to ensure all communities have improved access to safe drinking water, in a sustainable manner, for socio - economic development. The s ystems and processes of the Mo W R we re reviewed by the ACC as part of a general review of the practices of the water sector in 2021 and a separate report was l aunched in the first quarter of 2022. Systems and Processes Review (SPR) in Ministries Department and Agencies (MDAs) i s a corruption prevention intervention carried out to examine practices and procedures of public bodies to facilitate the discovery of corrupt practices or act s of corruption and to secure the revision of those practices and procedures which in the opinion of the Commission, may lead to or be conducive to corruption or corrupt practices. Recommendations proffered from systems reviews are meant to correct actio ns or lapses whether administrative, functional, or structural which may pose negative effects on the overall output of MDAs. The review was part of a holistic review of the Water Sector in Sierra Leone including the Sierra L e one Water Company (SALWACO) , Guma Valley Water Company (GUMA), the Ministry of Water Resources (MoWR) and the National Water Resource Management Agency ( NWRMA ) . The review focused on Budgetary Allocation and Utilization by these agencies a nd M inistry in the W ater S ector and separate reports were prepared and separately launched. Thus, this monitoring report only focuse d on gauging the compliance level of MoWR with the 43 recommendations proffered by the ACC R eview T eam. The idea of complian ce monitoring is consistent with the saying ‘what get s measured gets managed ’ (Drucker ) , 1954) ) . This simply means , examining an

20. - 15 - Stores had been relocated to a tidier location, providing an assistant for the Storekeeper and training provided for the S tores K eeper were not fully complied with. 7 .14 Internal Audit The Internal Audit Department implemented 3 out of 5 recommendations proffered by the R eview T eam recording a compliance rate of 60%. This was a disappointing situation, as the Internal Audit Unit was expected to be the promoter of compliance in the institution. Recommendations relating to the Conduct of a comprehensive audit and the increase in staff strength of the I nternal Audit Unit and the provision of logistics to the Internal Audit were not fully complie d with. However, Internal A udit queries are now responded to and implemented . 8 .0 CONCLUSION Based on the foregoing assessment, t he MoWR achieved a Moderate Compliance score of 65% that falls between the (50% - 79%) . compliance basket that do not moderate complian . In line with Section 4.3 of the CMSEPH, t he M anagement of the M inistry should be issued with a Warning Letter . to remind them of their obligation to comply. 9 .0 RECOMMENDATION We recommend that: 1. The Management of the MoWR expedites the implementation of the remaining 1 4 (3 8 – 24) applicable recommendations. 2. The ACC Commissioner cancels the Five (5) inapplicable recommendations highlighted in table 1 above. 3. Going forward, all MDAs especially the MoF that have stake and primary responsibility in the implementation of some recommendations proffered to

15. - 10 - 7 .1 Strategic Plan One (1) Recommendation was proffered by the systems and processes R eview T eam, and it was fully implemented indicating 100% compliance. This recommendation was concerned with the popularization of the S trategic P lan to all departments .Now all departments have identif ied their mandate in pursuing the overall mandate of the institution. The M inistry was able to align its S trategic P lan of 2019 - 2023 to the Medium - Term National Development Plan based on its activities and mandate and this was popularized to all departments in a retreat in Bo. 7 .2 Budget Preparation Four (4) out of five (5) recommendations proffered for this indicator have been fully implemented recording 80% compliance. The indicators fully implemented includes: the establishment of a functional B udget C ommittee, having a B udget O fficer, all activity plan s aligned to approved budget and maintaining a flex budget that will reflect actual budget disbursement. The remaining one recommendation that was not adhered to; representing 20% of the five (5) recommendations related to the participatory and inclusive budget process. 7 .3 Variance in Government Allocation and approved Budget Only one recommendation was proffered in this section, and it was not implemented. This implie d that the compliance score for this recommendation was 0 %. This according to Section 4.3 of the compliance sanction handbook of the ACC denotes Non - Compliance. However, the Principal Accountant of the Ministry informed the M onitoring T eam that instruction was beyond the management of the Ministry to implement. This was one of the Five (5) inapplicable recommendations highlighted in table 1 above.

16. - 11 - 7 .4 Delay in Government Allocation The recommendation concerning delay in government allocation was not complied with . This recommendation was also beyond the Ministry’s M anagement to implement, as the allocation of government funds was the responsibility of Central G overnment through the MoF and not the MoWR. This was one of the Five (5) inapplicable recommendations highlighted in table 1 above. 7 .5 Revenue Generation Two 2 out of two 2 recommendations proffered in the revenue generation indicator were not implemented. These have to do with the M inistry providing details of revenue generated and strengthening of revenue generation drive. The Ministry has not complied with these recommendations because; the MoWR was no longer a revenue generating Ministry. The revenue generation function, inclusive of the water Bowser had been transferred to the Ministry’s subsidiaries SALWCO and Guma Valley Water Company . These are 2 of the 5 inapplicable recommendations highlighted in table 1 above. 7 .6 Bowser Rental Systems review recommendations relating to the inclusion of penalty clause in subsequent contracts, amount owed to Chel e sco C ompany to be paid and the adherence to all contract agreement s have not been complied with . In the defense of the Energy Expert, wi th respect to the penalty clause, he stated that the project was no longer in the hands of the Ministry but GUMA Valley Water Company (GUMA) . Therefore , since the Ministry no longer implemented projects, the recommendation did not apply. This was one of the Five (5) inapplicable recommendations highlighted in table 1 above. Regarding the adherence to all agreements as recommended by the R eview T eam, the Energy Expert stated that all agreement s were adhere d to, but there was no evidence to substantiate his claim.

19. - 14 - March 2019 budget and the amount spent was within the budget. Thus, there was no need for a refund. Recommendation 29 - The sum of Le 20,000,000 should be accounted for as identified by the Internal Audit Annual report 2019, for annual WASH conference activities. Recommendation 30 - Le14,000,000 identified by the Internal A uditor in 2019 annual report with no supporting document to be refunded as Local training and workshop Recommendation 31 - All Expenditure s should be support ed with evidence. Now all expenditures undertaken by the M inistry are adequately supported with evidence. However, recommendations relating to the Development of a comprehensive retention policy, accounting for the variance in amount for local travelling and the accountability of variance in amount utilized on stationeries were not fully complied with . 7 . 12 Procurement M anagement All the two recommendations proffered by the Review Team were fully complied with, representing 100% compliance level. The recommendations relat ing to the keeping of Procurement document s within the office premises and staff leaving the M inistry making proper handing over note s have both been fully complied wit h. 7 .13 Stores Management 4 ( 80%) out of the five 5 recommendations raised in this indicator have been fully implemented . The recommendations complied with were Storekeepers taking goods on charge before distribution to sites and the Internal Audit Unit having representative that witness and/or verify all supplies.

9. - 4 - activity , changes the activity by forcing one to pay attention to it. Corruption opportunities can be managed and got rid of in MDAs if recommendations are implemented and appropriate sanctions levied for non - complian t situations. Against this backdrop, the ACC undertakes monitoring exercises to ensure compliance . This activity is critical as it compel s professionals and public officers in MDAs to plug loopholes that are conducive to the occurrence of graft. This report contains an alysis of findings on progress made by the MoWR in the implementation of ACC recommendation s . 2 . 0 AIMS AND OBJECTIVES The overall aim of this monitoring exercise was to measure the compliance level of the MoWR with the ACC Systems and Processes Review Recommendations. To achieve that aim, the key objectives were. To measure the compliance level of MoWR with the 43 ACCSPRR . To provide the ACC with insight on the effective utilization of public resources at MoWR . To Identify any barriers/issues, preventing and/or stalling the implementation of the SPRR for possible corrective intervention . To produce and present a report on the findings (compliance Level) and proffer recommendations for the ACC to take further act ions considering the relevant sections of the CMSE P H. 3.0 SCOPE & METHODOLOGY The M onitoring E xercise focused on verifying the impl ementation of the Forty - three (43 ) recommendations proffered by the Systems and processes Review T eam of the ACC . Corresponden ce in respect of an inception meeting was sent to and held with the M anagement of MoWR to ensure common understanding about the objectives, processes, and expected outcome s of the monitoring exercise.

18. - 13 - 7 . 9 With Holding Tax (WHT) 2 (100%) of the recommendation proffered in this indicator were fully implemented. Now Withholding Tax deductions are made at source, returns /schedules prepared and credited (paid) to NRA on time . Evidence of withholding tax deducted from payment made to service providers to the tune of Le 23,320,000 was presented and verified . 7 .10 Budget Line I tems and Activity plan (Budget Deviation) Two (2) out of three (3) recommendations proffered in this indicator have been fully implemented , recording 67% compliance. Among indicators fully implemented include: Alignment of the activity plan to the budget and maintaining a flex budget t hat reflect ed actual budget disbursement. Regarding the recommendation on the provision of document on vehicle maintenance to the M onitoring T eam has not been fully complied with; a receipt bearing the name of a garage; SUSCO MOTORS was shown to the T eam without the number of vehicles repaired. 7 .11 Financial Management The U nit had fully implemented four (4) out of eight (8) recommendations proffered by the R eview T eam; representing 50% compliance which denoted ‘ M oderate Compliance ’. Below are the recommendations that were fully implemented by MoWR: Recommendation 28 - The sum of Le 32,000,000 was expended on vehicle maintenance without a budget should be refunded. The M onitoring T eam had verified that this activity was budgeted for in Line 8 of the Ministry’s January to

6. - 1 - EXECUTIVE SUMMARY The Monitoring and Compliance Unit of the Prevention Department of the Anti - Corruption ( ACC ) undertook this exercise in August, 2022 to measure the compliance level of the Ministry of Water Resources (MoWR) with the ACC S ystems and Processes Review Recommendations (SPRR) in line with Section 8(1) of the A nti - Corruption Act (ACA) 2008 as a mended in 2019. Data analyzed showed that within three (3) months of receipt of ACC Systems and Processes Review recommendations the MoWR achieved 56 % Compliance Score, by fully implementing 2 4 out of the 43 recommendations proffered to the Ministry . Such a compliance score according to the Compliance Management and Sanctions E nforcement Procedure Handbook ( CMSEH) is termed as Moderate Compliance , which meant MoWR should be issued with a Warning Letter by the ACC to remind the M anagement of the M inistry of their obligation to fully comply with the remaining 19 (43 – 24) recommendation s . It is worth noting that 5 of the 19 outstanding recommendations, cannot be applied, or achieved by MoWR , because they were out of the control of the Agency. Had it not been for the 5 inapplicable recommendations, M o WR would have achieved a compliance score of 65 % by fully implementing 2 4 out of 37 applicable recommendation s and for which MoWR should still be issued with a Warning Letter for Moderately Complying with ACC ’s recommendations in line with Section 4.3 of the Compliance Management and Sanctions Enforcement Handbook (CMSEH). We recommend that: 1. The Management of the MoWR expedites the implementation of the remaining 1 4 (3 8 – 24) applicable recommendations. 2. The ACC Commissioner cancels the Five (5) inapplicable rec ommendations highlighted in table 1 below pursuant to Sect 8 (3) of the ACA 2008 as amended . 3. Going forward, all MDAs especially the Ministry of Finance (MoF) that have stake and primary responsibility in the implementation of some recommendations proffered

1. i MONITORING FOR COMPLIANCE WITH SYSTEMS AND PROCESSESS REVIEW RECOMMENDATIONS AT THE MINISTRY OF WATER RESOURCES BY: THE CORRUPTION PREVENTION DEPARTMENT – ACC AUGUST 2022

33. - 28 - 41 Management should provide adequate staff in the audit and provide logistics such as vehicles to perform their tasks # of internal audit staff added. provide logistics to Internal Audit H igh The Internal audit unit is understaffed with only two staff Two addition staff at the internal audit unit, Provide mobility to the Internal Audit unit. Verify additional personnel, job description, Mobile Logistics provide 0% The situation has worsened as there is now only one staff in the unit. The task that requires staff to use vehicles has not presented it. 42 Management should ensure that Audit is always present in verifying all deliverables before they are delivered, store and distributed # of goods verification conducted by Internal Audit The Audit Unit does not carry out physical verification Conduct goods verification before store Verify goods certification by Internal Audit. 100% The auditor is now al ways present to verify items delivered to stores and what is distributed. 43 The audit committee should be chaired by an external member who is knowledgeable in auditing. audit committee chaired by an external member who is knowledgeable in auditing H igh The Audit Committee was chaired by PS Audit committee chaired by an external member Verify minutes of Audit Committee 100% The PS is not a member or let alone a chair of the audit committee.

5. v | P a g e LIST OF ACRONYMS ACC Compliance Management and Sanctions Enforcement Handbook for Systems and Policy Review Recommendations ...... ...... ACCCMSEHSPRR ACC Compliance Progress Assessment Matrix ............ ........ .ACCCPAM Anti - Corruption Act ................................................ ....... . ACA GUMA Valley Water Company ................................. ..... GUMA Ministries Department and Agencies ........................ ...... MDAs Ministry of Water Resources .................................... .... MoWR Ministry of Fi nance ................................................ ... MoF Sierra L e one Water Company ................................. ..... SALWACO Systems and Processes Review .............................. ..... SPR Systems and Processes Review Recommendations ... .... SPRR

11. - 6 - 5.0 THE COMPLIANCE RATE (SCORE) The Compliance Score (CS) of the Agency is calculated as: Figure 2 : The Compliance Score 6.0 SUMMARY OF COMPLIANCE D ata analyzed showed that the MoWR within three (3) months of receipt of ACC SPRR had achieved 56% Compliance Score, by fully implementing 2 4 out of the 43 recommendations proffered to the Ministry. Such a compliance score according to the CMSE P H was termed Moderate Compliance , which mean t the MoWR should be issued with a Warning Letter 1 by the ACC to remind the Management of MoWR of their obligation to fully comply with ACC ’s instructions. It was however worth noting that 5 of the 19 (43 - 24 ) outstanding recommendations, sho wn in table 1 below , cannot be applied, or achieved by the MoW R , because they were out of the control of the Ministry . Table 1 below shows the 5 inapplicable recommendations. 1 A Compliance Score of 50% - 79% means Moderate Compliance. According to section 4.3 of the ACC Compliance Management and Sanctions Enforcement Handbook, a warning letter should be issued to the Ministry of Water resources reminding the management of the mi nistry of their obligation to comply with ACC r ecommendations as required by Section 8(1) of the ACC Act,2008 as amended in 2019. Compliance Score = Number of Recommendations Fully Implanted Total Number of Recommendations Proffere d 100

7. - 2 - The idea of compliance monitoring is consistent with the saying ‘What get measured gets managed’ by Peter Drucker. Corruption opportunities can be managed and rid of in MDAs if recommendations are implemented and appropriate sanctions are levied for non - compliance situations. Compliance Monitoring provides assurance to the ACC and the public in general about the achievement of th e objectives and benefits of systems and policies reviews in MDAs by gauging and reporting on the compliance scores of MDA with ACC Systems and Policies reviews recommendations . WHY COMPLIANCE MONIT ORING ? to MDAs, be invited to the presentation of Systems and Processes Review and Monitoring for Compliance reports.

14. - 9 - 7 .0 DETAILED FINDINGS AND ANALYSIS OF MINISTRY OF WATER COMPLIANC E Figure 3 : Double Column Chart showing the Compliance Levels of the various thematic Areas 1 5 1 1 2 3 4 1 2 3 8 2 5 5 4 1 2 4 4 3 Recommendations Proffered Recommendations Fully Implemented

10. - 5 - Key informants were interviewed, and documents were examined to triangulate the oral explanations in the implementation of the recommendations. Data on the impl ementation of the 43 recommendations w ere collected and recorded into the Compliance Progress Assessment Matrix (CPAM) . Ratings on the implementation of each of the recommendations w ere mostly participatory and based on verified evidence to mitigate subjectivity. An exit meeting was also held with the focal person and an agree ment was reached on the preliminary compliance score of the Ministry , which was not different from the final score. The Draft report was sent to the Management of the MoWR for the ir inputs and comments before the r eport was finalized. This process served as validation of the report prior to finalization, printing and launching. 4.0 THE COMPLIANCE BAROMETER Data was analyzed using the ACC’s Compliance Barometer with a scale of 0% - 100%. Figure 1 : The Compliance Baromet er 0% - 49% No Compliance (Indictment) 50% - 79% Moderate Compliance (Warning Letter) 80% - 90% Significant Compliance (Further Engagement) 90 % - 10 0% Significant Compliance ( Celebrated)

3. iii | P a g e TABLE OF CONTENTS EXECUTIVE SUMMARY ...................................................... ...................... . - 1 - 1.0 INTRODUCTION/BACKGROUND .................................... ..................... ... - 3 - 2 .0 AIMS AND OBJECTIVES: .................................................................. .... . - 4 - 3.0 SCOPE & METHODOLOGY ............................................................... .... . - 4 - 4 .0 THE COMPLIANCE BAROMETER ......................................................... .. . - 5 - 5 .0 THE COMPLIANCE RATE (SCORE) ........................................................ - 6 - 6 .0 SUMMARY OF COMPLIANCE ............................................................... . . - 6 - 7 DETAILED FINDINGS AND ANALYSIS OF MINISTRY OF WATER COMPLIANC - 9 - 7.1 Strategic Plan: .................................................................................. - 10 - 7.2 Budget Preparation: ............................................. .. ........................ ... . - 10 - 7.3 Variance in Government Allocation and approved Budget............... ....... ..... - 10 - 7.4 Delay in Government Allocation ...................................................... . ..... - 11 - 7.5 Revenue Generation: ........................................................................ . - 11 - 7.6 Bowser Rental ................................................................................. . . - 11 - 7.7 Fuel Management .............................................................................. - 12 - 7.8 Stipend to contract staff ............................................................... ..... .. - 12 - 7.9 With Holding Tax (WHT) ...................................................................... - 13 - 7.10 Budget Line items and Activity plan (Budget Deviation) ............................. - 13 - 7.11 Financial Management: ...................................................................... - 13 - 7.12 Procurement Management ............................................................... . ... - 14 - 7.1 3 Stores Management ......................................................................... - 14 - 7.1 4 Internal Audit.............................................................................. - 15 - 8 .0 CONCLUSION ................................................................................... - 15 - 9 .0 RECOMMENDATION .......................................................................... - 15 - 10.0 .A PPENDIXDATA CAPTURE AND REPORT MATRIX FOR MINISTRY OF WATER RESOURCES ............................................................................ . - 16 - LIST OF TABLES Table 1: The Five (5) Inapplicable Recommendations ........................................ - 7 -

13. - 8 - No. Baseline Recommendation Barrier preventing the implementation of the recommendation. provide details of such revenue. 4. No control or strengthen ing of revenue streams Strengthen the revenue generation drive to relax its over burden / reliance on Government support The Ministry was no longer generating revenue. The revenue generation function, inclusive of the water bowser ha d been transferred to the Ministry’s subsidiaries. No revenue generation to be strengthen ed . Area of Focus 5. The T eam realized that there was no penalty clause for breach of contract on the side of the buyer (the Ministry of Water Resources). Penalty clauses should be included in subsequent contract s the M oWR would enter as buyer of goods or services. The project had fold ed up. The sustainability/continuity of the project was now in the hands of the Guma Valley Water Company. Penalty clauses cannot be included in a project that has ended. Had it not been for those 5 inapplicable recommendations, the MoWR would have achiev ed a compliance score of 65% by fully implementing 2 4 out of 37 (43 - 5) applicable recommendation and for which the MoWR should still be issued a Warning Letter in line with Section 4.3 of the CMSE P H to remind the management of the MoWR of their obligation to fully comply with ACC recommendations . 65 % Figure 2 : The Compliance Score of the MoSW excluding the 5 Inapplicable 5 Recommendations

31. - 26 - 35 Management should ensure that the storekeeper should be provided with an assistant. Provide assistant for S torekeeper M No assistant for storekeeper One assistant for storekeeper Verify stores assistant, job description, duties and responsibilities 100% The recommendations have become obsolete as the S tores O fficer at the time has been re - designated and trans ferred to Government Printing D epartment. A new Stores and Inventory Management Officer from Finance is now in charge of stores with no stores assistant as the workload does not require that. 36 Provide required training for storekeeper in the discharge of his duties # of training provide for stores keeper M No required S tores training provided for stores personnel One training quarterly Verify training plan, report, attendance list & certificate. 100% 37 Storekeepers should be allowed to take goods on charge before distribution to sites. + Storekeepers took goods on charge before distribution to sites. H Most items procured were taken directly to site without going through stores No verification. Goods conducted by the stores and the internal audit. Storekeepers taking goods on charge before distribution to sites. - Sores ledger - Distribution list - verification and certification list. 100% Procured and other item purchase or otherwise by the Ministry p resently go through stores before distribution.

32. - 27 - 38 The Internal Audit Unit should have a representative to witness and/or verify all supplies. The Internal Audit Unit had representative that witness and/or verify all supplies. H The Internal Audit Unit to have representative that witness and/or verify all supplies. Verification R eports 100% The Internal audit and or representative now witness or verify all supplies received by stores. INTERNAL AUDIT Recommendations Indicator Import ance Baseline situation/ Challenges ACC’S Target Means of verification (MOVs) Current Progress Measure Responsible Department/Officer 39 Internal Audit plan should not be limited in conducting audit. Conduct comprehensive audit. H Audit unit is restricted in in executing activities contained in the audit plan. Conduct comprehensive audit Verify audit implementation plan. 80% Five out of the seven activities in the AWP were executed for 2021. While none of the four activities in the plan for 2022 has been executed due to unavailability of funds and the conduct of external audit. 2022: There are four activities in the audit plan that should be conducted by the audit 40 Management should adhere to Internal audit * recommendations proffered. # of Internal audit queries responded and implemented H igh Internal Audit queries are not adequately responded to as management seems not to treat the report with utmost importance. Implement all internal audit queries Verify management response, internal audit report final. 90% Management is now adhering to internal audit recommendations, though at a very slow pace.

12. - 7 - Table 1 : The Five (5) Inapplicable Recommendations No. Baseline Recommendation Barrier preventing the implementation of the recommendation. Area of Focus: Variance in Government Allocation and Approved Budget 1. No further details with regards the adverse budget variance of Le173,149,000 (one hundred and seventy - three million, one hundred and forty - nine thousand Leones . M o F should provide adequate funds in line with the budget are provided to the institution. Letters were written by the Ministry to MoF following up on the difference of Le173,149,000 between the budget approved and amounts received, but no response was received. The public body with direct responsible in this recommendation was the MoF. Theref ore, it cannot be implemented by MoWR . Area of Focus: Delay in Government Allocation 2 . Delays in the disbursement of funds from the Ministry MoF to the M oWR The Government of Sierra Leone (GoSL) through the M oF should ensure that quarterly allocations (actual) are disbursed on time. Every MDA in Sierra Leone would love to receive its quarterly allocation on time. That was not the case in Sierra Leone. Again, the public body with direct responsib ility in this rec ommendation was MoF . Therefore, it cannot be implemented by MoWR. Area of Focus: Revenue Generation 3. There was no evidence presented to show that the M inistry generate d revenue even though it possesse d Water Bowsers/tankers that supply water externally on commercial basis. The Finance unit of the M inistry should provide details of all revenue generated activities of the M inistry inclusive of water bowser. The Ministry no longer generate d revenue. The re venue generation function, inclusive of the water bowser ha d been transferred to the Ministry’s subsidiary Agencies SALWACO and GUM A and was not certain that it will receive any revenue from them. Therefore, the MoWR can no longer 56% Figure 1 : The Compliance Score of the MoSW Including the 5 Inapplicable 5 Recommendations

25. - 20 - 12 The sum of Forty - four Million (Old Leone 44,000,000) equivalent to NSL 44,000 to be paid to Chelesco Company % of amount paid to Chelesco Company H igh Outstanding balance payment of NSL 44.000 was not paid to Chelesco Company. 100% payment of all outstanding balance Verify payment slip. 50% A request was made by the project engineer to the Ministry of Finance for the payment of the said amount. But it was not honored by MoF because the MoF will only considers bad debts payments when it is Le 1 billion and above. 13 The M inistry should ensure that all agreement stated in any contract documents adhered to # of agreement contract documented H igh Agreement contracts were not adhered to by the ministry of water resources agreement contract documented adhered to. Verify current agreement contract and its implementation. 0% A claim was made on a project been i mplemented with all agreement in the contract document adhered to. But evidence of that was not presented to the team. FUEL Recommendations Indicator Impor tance Baseline situation/ Challenges ACC’S Target Means of verification (MOVs) Current Progress Measure Responsible Department/Officer 14 The excess fuel of 285 liters misused and/or misappropriated on vehicles amounting to Le2,137,500 (Two Million One Hundred and Thirty - Seven Thousand Five Hundred Leones) through unlawful fueling of two extra vehicles should be accounted for. % of money accounted from the excess of 285 liters misuse H igh An excess fuel of 285 liters was misused and/or misappropriated on vehicles amounting to Le 2,137,500 (Two Million One Hundred and Thirty - Seven Thousand Five Hundred Leones) through unlawful fueling of two extra vehicles. 100% refund of excesses amount misuse. Verify payment slip a nd supporting document 0% No action taken with respect to this recommendation.

27. - 22 - WITH HOLDING TAX (WHT) Recommendations Indicator Import ance Baseline situation/ Challenges ACC’S Target Means of V erification (MOVs) Current Progress Measure Responsible Department/Officer 19 Tax obligations should be honored as stipulated by law. Tax obligations honored as stipulated by law. H igh It was observed that withholding tax deductions are done at the ministry of Finance and the deducted tax amount is credited to NRA’s account at the Bank of Sierra Leone. Tax obligations to be honored as stipu lated by law. Tax payment Tax schedule 100% The Ministry now paid all withholding tax to NRA. Evidence of tax payment such as the payment of withholding tax on services to the tune of Le 23,320,000 was provided to the Monitoring T eam. 20 WHT deductions should be deducted at source and returns credited to NRA. WHT deductions are deducted at source and returns credited to NRA. H igh Withholding tax are not deducted WHT deductions are to be deducted at source and returns credited to NRA. Tax payment Tax schedule 100% There is evidence of withholding tax been deducted from payment on services to the tune of Le23,320,000. BUDGET LINE ITEMS AND ACTIVITY P LAN (BUDGET DEVIATION) Recommendations Indicator Impor tance Baseline situation/ Challenges ACC’S Target Means of verification (MOVs) Current Progress Measure Responsible Department/Officer 21 Management should ensure that all activity planned are in line with the approved budget. Alignment of planned activities and approved budget is ensured by management. H igh It was discovered that Le32,000,000 ( thirty - two million Leones) was expended for vehicle maintenance without being part of the budget. Alignment of planned activities and approved budget is to be ensured by management. Planned activities A pproved budget 100% Activity plans are now in line with approved budget.

29. - 24 - 26 The sum of 43,000,000 to be accounted for as amount paid to Davidne Dimension Ent and Diaco investment with no supporting documents provided to the team as stationary procure. % of variance amount utilize for S tationaries accounted for. H igh No supporting documents provided for the utilization of 43,000 ,000 for stationary 100% Compliance Verify payment slip, Bank statement 61% Supporting document is now provided for the Le26,310,000. Balance of Le 16,690,000. 27 The sum of Le 32,000,000 was expended on vehicle maintenance without budgeted should be refunded. % of variance amount utilize for vehicle maintenance H igh No supporting documents provided for the utilization Le 32,000 ,000 for Vehicle maintenance 100% Maintenance Verify payment slip, Bank statement 100% The activity is in the budget. 28 The sum of Le 20,000,000 should be accounted for as identified by the Internal Audit Annual report 2019, for annual WASH conference activities. % of variance amount utilize for annual wash conference activities H igh No supporting documents provided for th e use of Le 20,000 ,000 for WASH Conference 100% Compliance Verify payment slip, Bank statement 100% The internal audit report provided evidence of the issue been resolved. 29 14,000,000 identified by the Internal auditor in 2019 annual report with no supporting document to be refunded as Local training and workshop % of variance amount use for Local training and workshop with no supporting documents H igh No supporting document s provided for the use of Le 20,000 ,000 for local training 100% Compliance Verify payment slip, Bank statement 100% The internal audit report provided evidence of the issue been resolved. 30 All Expenditure should be support with supporting documents. % of Expenditure with supporting documents H igh No supporting Document on Expenditure undertaken. All Expenditure supported with supporting documents. Verify expenditure proposals and payments. 100% A couple of expenditure were sampled, and they are with the necessary supporting document.

22. - 17 - Area of Focus STRATEGIC PLAN Anti - Corruption Objectives Institute T ransparency and A ccountability P rinciples in the M anagement of P ublic F unds Recommendations Indicator Impor tance Baseline situation/ Challenges ACC’S Target Means of V erification (MOVs) Current Progress Measure Responsible Department/Officer 1 The Ministry should popularize the strategic plan to all departments, in a view that all department identifies its mandate in pursuing the overall mandate of the I nstitution Popularize S trategic P lan to all departments High There was no Strategic Plan presented to the Review Team. I nclusive input of all departments in the S t rategic P lan Verify approved S trategic P lan, inputs of all Departments and Units 100% The S trategic P lan was aligned to the Medium - T erm National Development Plan based on her mandate and popularized to all departments in a retreat in Bo . BUDGET Recommendations Indicator Import ance Baseline situation/ Challenges ACC’S Target Means of V erification (MOVs) Current Progress Measure Responsible Department/Officer 2 Budget process to be highly participatory inclusive of all departments to prepare plans for its proposed activities for the budgeting period Participatory and inclusive budget process. H igh Budget processes is not participatory but rather limited to the executive body Participatory and Inclusive Annual Budget Verify Inputs of Department and Unit budget submitted. 85% The budget process was participatory as all the various parties at HQ are brought to a round table discussion of the budget during it preparation. But there was no evidence of departmental/unit budget submission to the Budget Officer, besides that coming from the Directorate of Water Resources. 10 .0 APPENDIXDATA CAPTURE AND REPORT MATRIX FOR MINISTRY OF WATER RESOURCES YEAR OF REVIEW - 2021 PROGRESS ASSESSMENT TOOL& COMPLIANCE BAROMETER

26. - 21 - 15 The variance of Le129,377,000 resulting from the difference between expenditure on fuel and verified amount by the Review team should be accounted for. % of amount variance accounted for. H igh A total of Le 129,377,000 could not be accounted for fuel usage. This resulted from the variance between amount spent on fuel and that verified by the team. 100% payment of variance paid . Verify Receipt of payment, Bank Statement. 0% No action taken with respect to this recommendation. 16 Supporting documents ( logbooks , fuel register, invoices, receipts, etc.) should be provided to the team with respect to the amount spent on fuel. Fuel Accountability tools provided. H igh No supporting documents ( logbooks , fuel register, invoices, receipts, etc.) were provided to the team with regard the amount expended. All fuel accountability tools provided. Verify logbooks , fuel register, invoices, receipts, fuel ledger. 100% Sample of fuel register, payment vouchers and receipts were provided and inspected. 17 Fuel abuse should be controlled with a robust fuel reconciliation report and tracking plan Fuel reconciliation report developed. No fuel reconciliation report Monthly fuel reconciliation report Verify Fuel reconciliation report. 80% Despite the project has fold up, the finance department has developed a fuel policy. This policy is expected to be implemented in such a way that fuel can be used judiciously through robust fuel reconciliation and tracking plan STIPEND TO FULL TIME STAFF Recommendations Indicator Import ance Baseline situation/ Challenges ACC’S Target Means of V erification (MOVs) Current Progress Measure Responsible Department/Officer 18 MWR) full time staff should not be receiving stipend away from their salary for the same job that they are recruited for it is an act of double dipping. (# of full - time staff involved in project receiving stipend H igh It was discovered that most and /or all the contract staff receiving stipends are full time employees of the various institutions (GWVC and MWR). No stipend for full time staff for performing the same job that were recruited for. Staff list of ( GWVC and MWR) Payroll of (GWVC and MWR) 100% The project has fold up and the Ministry of Water Resources is only left with the supervisory roles which do not require staff to be contracted by her subsidiaries. Thus , full time staff of MoWR do not currently receive any stipend for same job.

28. - 23 - 22 Document with regards to vehicle maintenance should be provided to the team. For instance, name of garage, number of vehicles maintenance, payment vouchers and receipts. Document with regards to vehicle maintenance provided to the team. For instance, name of garage, number of vehicles maintenance, payment vouchers and receipts. H igh No document with regards to vehicle maintenance was provided to the team. For instance, nam e of garage, number of vehicles maintenance, payment vouchers and receipts. Document with regards to vehicle maintenance to be provided to the team. For instance, name of garage, number of vehicles maintenance, payment vouchers and receipts. Documents such as name of garage, number of vehicles maintenance, payment vouchers and receipts. 50% A receipt bearing the name of a garage; SUSCO MOTORS was shown to the team without the number of vehicles maintenance and payment vouchers. 23 In cases of variances in budget funds, the budget should be revised, and activity plan should be line with the revised budget. In cases of variances in budget funds, the budget is revised, and activity plan aligned with the revised budget. H igh It was observed that In cases of adverse budget, activity plans are rarely in line with approved budget. In cases of variances in budget funds, the budget is to be revised and activity plan aligned with the revised budget. Budget Activity plan revised activity plan 100% The ministry now has a flex budget when there is a variance between budget and allocation thus activity plan were aligned to the revised budget. FINANCIAL MANAGEMENT Recommendations Indicator Import ance Baseline situation/ Challenges ACC’S Target Means of V erification (MOVs) Current Progress Measure Responsible Department/Officer 24 Management should have a comprehensive document retention policy. Developed a comprehensive retention policy H igh There was no comprehensive retention policy Approved Comprehensive retention policy crafted. Physical verification of approved retention policy. 80% A draft retention policy is in place, awaiting finalization and management approval. 25 The variance of 16,850,000 to be accounted for as local travelling with no supporting documents such as approval budget proposal, reports, and retirement. % of variance amount for local travelling accounted for H igh No supporting documents provided for the utilization of 16,850 ,000 as travelling 100 % Compliance Verify payment slip, Bank statement 0% The transaction was traced but cannot be found.

30. - 25 - 31 We recommend that monthly Bank Reconciliation be prepared for all bank accounts maintained by the Ministry and such reconciliations should be reviewed by the head of the Finance Office. M onthly Bank Reconciliation prepared for all bank accounts maintained by the Ministry and reviewed by the head of the Finance Office. H igh Monthly Bank Reconciliations statements were not prepared by the Finance Officer. M onthly Bank Reconciliation prepared for all ban k accounts to be maintained by the Ministry and reviewed by the head of the Finance Office. Bank reconciliation statement 85% Bank reconciliations were done but not reviewed by the Principal Accountant. As they were not signed. PROCUMENT MANAGEMENT Recommendations Indicator Import ance Baseline situation/ Challenges ACC’S Target Means of V erification (MOVs) Current Progress Measure Responsible Department/Officer 32 A system should be established that prohibit document to be in the sole custody of individual rather than filed at the office premises. % of Procurement document kept within the office premises. H igh Procurement documents were not kept within the office Procurement document kept within the office premises. Verify Procurement document file within the procurement office. 100% The procurement documents are now kept in the P rocurement office 33 All staff leaving the Ministry should do proper handing before proceeding. # Of staff leaving the ministry with proper handing over note M No proper handling over done by staff before proceed on leave. Proper handing over done to staff before proceeding on leave. Verify # of staff proceed on Leave that done Handling over notes 100% The recommendation has been adhered to as, there was a formal h anding over note presented to the incoming Senior procurement officer. STORES MANAGEMENT Recommendations Indicator Importa nce Baseline situation/ Challenges ACC’S Target Means of V erification (MOVs) Current Progress Measure Responsible Department/Officer 34 Management should relocate the stores to a tidier location, Stores relocated to a tidier location. M The Store is not tidily kept though spacious as it is in a disaster - prone area, and it floods during the rains. Stores to be relocated to a tidier location. R elocated stores 0% The store is still where it is located and in a dilapidated condition.

24. - 19 - DELAY IN GOVERNMENT ALLOCATION Recommendations Indicator Import ance Baseline situation/ Challenges ACC’S Target Means of V erification (MOVs) Current Progress Measure Responsible Department/Officer 8 The Government of Sierra Leone (GoSL) through the Ministry of Finance (MOFED) should ensure that quarterly allocations (actual) are disbursed on time. # of quarterly allocation disbursed to NWRMA L Delays in the disbursement of funds from the Ministry of Finance to the Ministry of Water Resources. Quarterly allocation of funds Verify Actual disbursement of funds as against budget, 0% Funds were not provided on time. Sometimes they are even not provided for a quarter or more and this is not within their control. No evidence provided. REVENUE GENERATION Recommendations Indicator Importa nce Baseline situation/ Challenges ACC’S Target Means of V erification (MOVs) Current Progress Measure Responsible Department/Officer 9 The Finance unit of the ministry should provide details of all revenue generated activities of the M inistry inclusive of water bowser. # of revenue streams identified in the M inistry. H igh There was no evidence presented to show that the ministry generates revenue even though it possesses Water Bowsers/tankers that used to supply water externally on commercial basis . Identified all revenue generated accounted for the period under review/moni toring revenue streams identified Revenue generated and evidence of payment slips, bank statement, records of cash book. 0% The Ministry is no longer generating revenue. The revenue generation function, inclusive of the water bowser has been transferred to the Ministry’s subsidiaries . 10 Strengthen the revenue generation drive in order to relax its over burden reliance on Government support Strengthen the revenue generation drive. H igh No control or strengthen of revenue streams Revenue generation strengthen Verify mechanism in place to strengthen revenue 0% The Ministry is no longer generating revenue. The revenue generation function, inclusive of the wat er bowser has been transferred to the Ministry’s subsidiaries . BOWSER RENTAL Recommendations Indicator Impor tance Baseline situation/ Challenges ACC’S Target Means of verification (MOVs) Current Progress Measure Responsible Department/Officer 11 Penalty clauses should be included in subsequent contract of the Ministry of Water Resources is entering into as buyer of goods or services. Penalty clauses included in subsequent contracts entered by the Ministry, when serving as a buyer. H igh The team re alized that there is no penalty clause for breach of contract on the side of the buyer (the Ministry of Water Resources). Penalty clauses included in subsequent contracts entered by the Ministry, when serving as a buyer. Verify Subsequent contracts 0% The project has fold up. The sustainability/continuity of the project is now in the hands of the Guma Valley Water Company.

23. - 18 - 3 The M inistry should immediately constitute a Budget Committee Comprising of all Heads of Departments of the board with the free hand to guide the budget process Establishment of approved budget committee H igh No budget committee to guide the budget process. Approved and functional Budget Committee Verify List of Budget Committee, updated Minutes of the committee, resolution, and Budget work plan 100% There is now a budget committee that is made up of representatives of the various departments in the Ministry. Evidence of the F inance C ommittee shared with the team, such as minutes and attendance. 4 The Ministry together with the Budget Bureau should ensure a stationed Budget Officer assigned. Assigned Budget officer H igh No assigned Budget Officer in the Ministry Assigned One Budget Officer Verify appointment letter or correspondence of designation of Budget office, Job description roles and responsibility. 100% A stationed Budget Officer from Budget Bureau has been assigned to the M inistry since 15 th March , 2021. Since then, there has been progress in facilit ating the budget process in the M inistry. 5 All activity plans should be in line with approved budget. Activity implemented in line with approved budget H igh Activity implemented not in line with activity plan Activity implemented in line with approved budget Verify Plan activity, in line with activity implemented report 100% Activity plans are now in line with approved budget. 6 Variance in budget funds the budget should be revised, and the activities plan should be in line with revised budget. # of activity implemented in line with revised budget H igh Activity implemented are not in line with revised budget Activity implemented in line with approved budget Verify Plan activity, in line with activity implemented report 100% The M inistry now has a flex budget when there is a variance between budget and allocation thus activity plan was aligned to the revised budget . VARIANCE IN GOVERNMENT ALLOCATION AND APPROVED BUDGET Recommendations Indicator Import ance Baseline situation/ Challenges ACC’S Target Means of V erification (MOVs) Current Progress Measure Responsible Department/Officer 7 MOF should provide adequate funds in line with the budget are provided to the institution. Adequate fund in line with budget provided to the institution. L No further details with regards th e adverse budget variance of Le 173,149,000 (one hundred and seventy - three million, one hundred and forty - nine thousand Leones). All variances are to be properly investigated to determine its cause and remedy taken by Government All variances should be properly investigated to determine its cause and remedy taken by Government. 0% There is still an adverse variance between budget and disburseme nt from MoF. However, evidence to support this claim was not provided to the team.